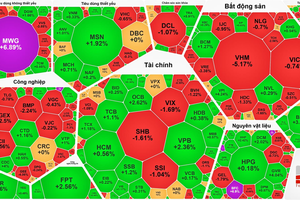

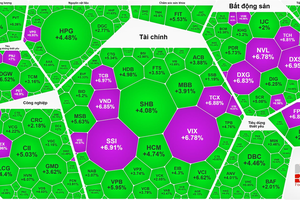

The information was disclosed in a newly released report by SSI Research. The revised list features a heavy concentration of financials (banking and securities) and real estate names, including STB, VCB, BID, SHB, SSI, VIX, VCI, VND, VIC, VHM, VRE, NVL, and KBC. It also comprises a range of other large-cap stocks such as HPG, FPT, MSN, VNM, VJC, GEX, KDH, DGC, BSR, and GEE.

At the same time, Vietnam’s weighting across FTSE index families has been revised downward based on data as of March 31, 2026. Specifically, its weight in the FTSE Global All Cap Index fell from 0.037 percent to 0.034 percent; in the FTSE Emerging All Cap Index from 0.350 percent to 0.329 percent; in the FTSE All-World Index from 0.024 percent to 0.020 percent; and in the FTSE Emerging Index from 0.227 percent to 0.192 percent.

The official list is expected to be released ahead of the FTSE GEIS index review in September 2026, with changes from this semi-annual review likely to be announced starting August 21, 2026.

SSI Research estimates that total inflows from FTSE-tracking exchange-traded funds could reach approximately US$1.3 billion, with the Vanguard FTSE Emerging Markets ETF projected to account for the largest share at around US$481 million.

In terms of disbursement, capital flows are forecast to be phased across four stages: 10 percent in September 2026, 20 percent in March 2027, 35 percent in June 2027, and the remaining 35 percent in September 2027 - equivalent to roughly US$130 million, US$260 million, and two tranches of US$455 million each.

By individual stock, VIC is expected to lead in both market capitalization and estimated inflows at about US$498 million, equivalent to roughly 14.6 trading days. Other major beneficiaries include HPG (US$115 million), VHM (US$99 million), FPT (US$69 million), and MSN (US$63 million).

SSI Research also noted that Vietnam stands a strong chance of being placed on the watch list in MSCI’s June 2026 review, which applies more stringent criteria. The Vietnamese stock market has so far met 10 out of 18 market accessibility requirements under MSCI’s framework and continues to improve on the remaining metrics. This is widely seen as a critical stepping stone toward a formal upgrade to emerging market status.