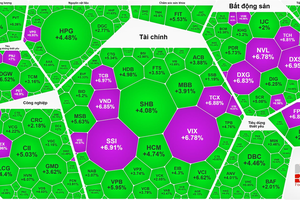

Vietnam’s stock market has entered a transformative phase after being reclassified by FTSE Russell as a secondary emerging market, a milestone expected to unlock tens of billions of U.S. dollars in foreign investment and accelerate regulatory reforms. Several recently issued and upcoming policies are expected to further accelerate this momentum, paving the way for substantial inflows of international capital.

Attracting foreign capital

In October 2025, FTSE Russell, one of the world’s three leading index providers, announced that Vietnam had been upgraded from Frontier Market to Secondary Emerging Market, effective in 2026.

According to Wanming Du, FTSE’s Director of Index Policy, Vietnam has met all nine criteria required for secondary emerging market classification under FTSE’s global standards.

Tran Anh Dao, Acting CEO of the Ho Chi Minh Stock Exchange (HOSE), emphasized that the market upgrade represents a major opportunity for Vietnam to attract new, more stable, and sustainable sources of capital potentially worth tens of billions of U.S. dollars. However, she noted that improving corporate governance remains critical for Vietnam to join the top five ASEAN countries with the best governance practices.

To address barriers to market upgrading and protect foreign investors’ interests, the Government issued Decree 245/2025 on September 12, 2025, abolishing the rule that allowed public companies to set their own foreign ownership limits. This change expands market accessibility for foreign investors.

In November 2025, the Ministry of Finance issued Decision 3761/2025, detailing the implementation of Decree 245/2025. It tasked the Foreign Investment Agency with coordinating the State Securities Commission and relevant agencies to review business sectors subject to conditional foreign investment and propose lifting or relaxing ownership restrictions in non-sensitive industries.

Previously, foreign ownership in Vietnamese companies depended on industry regulations typically capped at 50 percent or 100 percent. Allowing companies to self-set their foreign ownership ratio led some firms to impose very low limits (as little as 5–10 percent) to prevent takeovers or protect controlling shareholder groups.

Under the new rules, only companies that have already announced their ownership limits may retain or adjust them, provided they publicly disclose and complete necessary procedures within 12 months. The Vietnam Securities Depository and Clearing Corporation (VSDC) will publicly update each company’s maximum and current foreign ownership levels on its website.

Pilot program for short selling

Alongside foreign ownership reform, the Ministry of Finance has issued Decision 2014/2025 to implement the Market Upgrading Project, focusing on three key pillars including regulated short selling, securities borrowing and lending (SBL), and same-day (T+0) trading. These core operations are scheduled for rollout between 2026 and 2028.

Short selling allows investors to sell shares they do not own by borrowing them from a broker or lender, profiting from anticipated price declines. Investors sell borrowed shares at current high prices, then repurchase them later at lower prices to return to the lender, capturing the price difference as profit.

Tran Duc Anh, Director of KB Securities Vietnam’s Macroeconomics and Market Strategy Division, noted that Vietnam currently only allows short-selling-like strategies in the derivatives market through two-way transactions. Establishing a regulated short-selling mechanism is a crucial government initiative to elevate Vietnam’s capital market to international standards of transparency, efficiency, and sustainability.

“Short selling is a milestone that helps markets operate more efficiently and reflect true value. When stocks are overinflated, short-selling pressure brings prices back to fair value, reducing the risk of bubbles. It also serves as a hedge during volatile periods,” Tran Duc Anh explained.

Economist Pham Tien Dat of the Institute for Financial and Economic Policy Strategies added that international experience shows short selling works best under a rigorous, transparent, and flexible risk management framework. Vietnam must require strong financial capacity and risk control from brokerage firms, limit eligible short-selling stocks to large-cap, highly liquid groups, and maintain robust monitoring and enforcement mechanisms. Temporary restrictions may be imposed during extreme volatility, but excessive market intervention should be avoided.