|

However, the subsequent rebound revealed the fragility of cash flow as numerous astute investors opted to cash in their profits and observe from the sidelines. It appears that the lesson of over-optimism has yet to be internalized by a significant portion of investors.

The Stock Market's Infallibility Falters

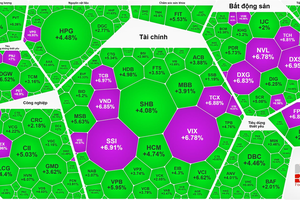

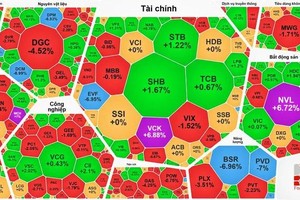

Up until August 16, when the VN-Index surged to 1,243.26 points - the highest in the first eight months of 2023 - a slew of companies remained steadfastly bullish about the growth trajectory. At that juncture, the anticipated culmination of the uptrend was pegged at 1,300 points for August. Across investment groups and online forums, enthusiastic endorsements urging investors to purchase further stoked the flames of greed.

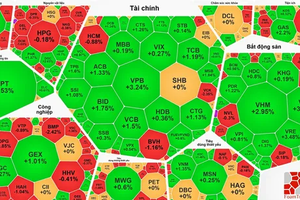

Amidst the zenith of optimism, the stock market underwent a dramatic reversal, experiencing its most considerable shock drop since early May 2022. This decline of over 55 points within a single day was an exceedingly rare occurrence, reminiscent of the market's slump following the historic peak in April 2022.

The aftermath of this precipitous drop was dissected exhaustively, with even several securities companies, previously bullish, suddenly altering their stance and asserting that the market correction was both reasonable and requisite. Endeavors to rationalize this cyclic phenomenon underscore that all assessments are fundamentally propelled by sentiment, with analysts ultimately unable to break free from the standard psychological state governing trading.

If one had to pinpoint the stock market adage that has led to the most investor "casualties," it would undoubtedly be "The market is always right." No investor steps into the market without this adage etched into their consciousness. However, after undergoing numerous market fluctuations, investors invariably realize that the market is not infallible. This realization arises due to the market's composite nature, driven by a blend of avarice and trepidation.

Curiously, when the market is most exuberant and optimistic, with everyone reaping profits, that is precisely the juncture at which the market becomes fallible. It's no coincidence that during each historical market peak, transactions surge to a fever pitch, with liquidity reaching its zenith. This surge results from investors exhaustively investing their available capital while simultaneously leveraging to the maximum.

The Ebb and Flow of a Prolonged Game

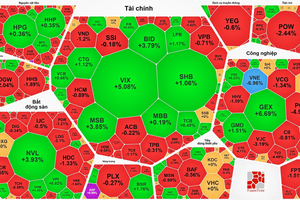

Currently, even as numerous investors found themselves compelled to divest their stocks last week, many still walked away with gains. This phenomenon is a consequence of the burgeoning margin, rendering it feasible to yield returns of a few dozen percentage points to the market. Only those investors ensnared at the market's apex will truly bear the brunt of losses.

For the multitude of investors who have entered the market within the past three months (comprising over 400,000 new accounts opened between May and July), this might represent a "sugar-coated bullet." Yet, it's essential to recognize that repeating errors is all too plausible during forthcoming market cycles. Joining amidst an explosive growth phase tends to make almost any stock purchase profitable.

However, effective stock investment transcends attaining victories in individual trades at distinct market stages; it hinges on discipline and a well-defined strategy. What few investors grasp is that investment decisions are more often incorrect than correct, with each decision entailing a gamble accompanied by risk. The adage "high risk, high return" is often misconstrued to signify accepting substantial risks to secure substantial profits, placing emphasis on the latter (substantial profits). In actuality, the reverse is true: risk should be at the forefront, assessing whether the anticipated returns for a given risk level are commensurate.

This counterintuitive perspective becomes particularly apparent when examining leverage. Margin inherently involves perilous capital (involving interest payments and collateral) and is ideally suited for ultra-short-term speculation (given that the longer the period, the more challenging it becomes to predict stock price and market shifts). Nonetheless, numerous investors embrace extraordinarily elevated leverage ratios—such as 2:8 or 3:7—and engage in long-term holdings. They willingly shoulder elevated risks, aspiring for substantial gains while occasionally attaining them in individual transactions. In essence, the higher the leverage employed, the greater the peril of loss due to incorrect decisions outweighing correct ones, and erroneous timings being magnified due to borrowed funds.

Consequently, the crux of a sound investment strategy rests on prioritizing risk management prior to pursuing profits—limiting losses stemming from erroneous decisions. This approach necessitates a long-term outlook, even if it entails foregoing the multiplied returns accompanying single deals.