Illustrative photo

Illustrative photo

Even if one blames the US Federal Reserve (FED) interest rate hike, it only caused the S&P 500 to drop 9.3 percent. One cannot either look to blame the gas crisis, although it increased the risk of a recession, and only sent German stocks down by 5.5 percent. The situation of the stock market in Vietnam is currently causing a headache for many investors, especially when the GDP growth rate in Vietnam in the third quarter was amongst the strongest in the world.

Unusual phenomenon

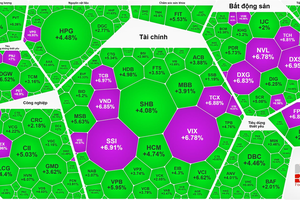

At the end of the first trading week in October, the VN Index fell to the bottom of twenty months but then started to recover. The signs of bottom formation appeared at the end of the third quarter when listed companies were preparing to publish their financial statements. In the short term, this is the only supportive information the market can expect.

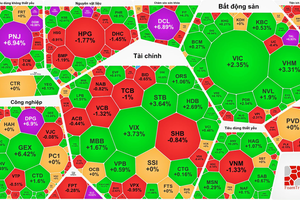

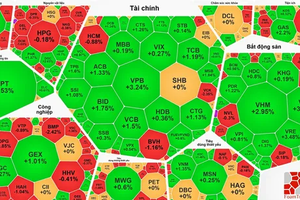

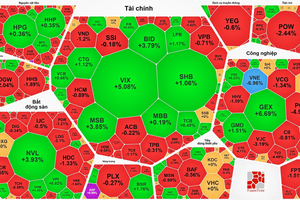

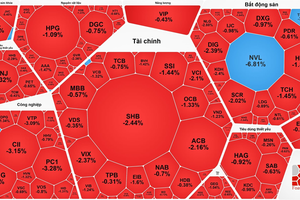

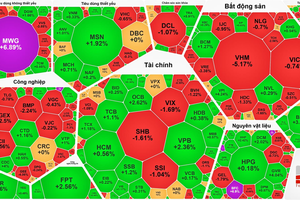

A distinctive feature of the stock market in the third quarter financial statement of this year was that the market did not have a normal accumulation period before. Market practices in previous years have shown that the movement of smart cash flow precedes the opportunity for businesses to announce profits. This year in September, almost the whole market fell, and even stocks dropped sharply. Even with the blue chips in the VN30 basket, there were 20 stocks that lost 10 percent or more in value since the beginning of September. Among these were a series of stocks that have fallen over 20 percent, namely, CTG was down by 21.3 percent, GVR was down by 27 percent, HPG was down by 20 percent, KDH was down by 25.3 percent, MSN was down by 20.8 percent, PLX was down by 21.2 percent, SSI was down by 21.3 percent, STB was down by 22 percent, and TCB was down by 21 percent.

This drastic drop in some respects represents an opportunity to buy cheap, but in other respects, it is an unusual phenomenon. The large discount margin exceeded the normal correction by about 7 percent to 10 percent, showing the view of the market that the stock is revaluing and not simply correcting after the previous growth. Indeed, if calculated from the lowest bottom in July after the market reflected the business results of the second quarter of 2022, a series of stocks broke through this bottom similar to the VN Index and fell to a new low in the last many years. This development reflects further risks, which will be difficult to see by only looking at current data.

The most obvious example is the group of financial stocks as mentioned above, which are in the group with the strongest decline. Securities stocks are forecast to have a dismal third quarter when the overall liquidity level will decrease by about 60 percent compared to 2021. This means that the growth rate of brokerage income will be reduced, as well as the risk of the portfolio incurring losses. Proprietary activities account for about 50 percent of the total revenue of securities companies, and when the majority of stocks plummet, it will be difficult to expect this profit to reflect a positive number in the third quarter financial statements. Although bank stocks can share savings to ensure profits, the prospect of raising deposit rates while limited lending space will reduce profit margins, along with difficult bond trading activities.

For business groups, the impact on profits can be very different, but it is also difficult to avoid the general downward psychological pressure in the market. These are the stocks that have great room for investors according to the fundamentalist school, but they are the stocks that do not have much impact on the overall market trend because the capitalization is too small, or the industry does not spread in price. This will create a divergence in stock prices in the market, and it is likely that this year will have an unusual third quarter when the short-term profit story depends mainly on whether investors choose the right stocks or not, along with whether those stocks attract large enough cash flow to increase the price or not. Therefore, it is difficult to say that the third quarter business results will be the general support for the whole market, forming the so-called financial report wave.

Unpredictable future

A less noticeable change in recent stock market outlook reports is that the forecast earnings growth figures for 2022 of listed companies are decreasing. In the first two quarters of the year, many forecast profit growths of 20 percent to 25 percent, but this number is gradually shrinking from 18 percent to 20 percent, or even 15 percent to 17 percent. This rather subtle change implies that profit growth in the last two quarters of this year will be difficult to grow, even see reduced growth. The data of the third quarter will be the premise for many more downgrades to appear.

The stock market may be discounting medium-term risks when the best is over. The statistics always reflect the past, such as the record GDP growth of 13 percent just announced, while the market is ready for changes for the worst in the future. Even international organizations, although very optimistic for 2022, remain still cautious in 2023. For instance, in the recently released report of UOB Bank, although they raised Vietnam's GDP growth forecast from 7 percent to 8.2 percent in 2022, they still emphasized the pressure of increasing global interest rates on Vietnam's operating policy in 2023, as well as the risk of recession in the main export markets, the EU and the US.

The objectives are somewhat contradictory such as curbing inflation, maintaining growth, supporting interest rates, stabilizing exchange rates to keep investment capital flow, and limiting imports of inflation, thereby making policy selection difficult. The State Bank of Vietnam is determined not to increase the credit ceiling, raise the operating interest rate, and loosening the ceiling deposit interest rate to achieve the current balance. However, that is only the first half of the fight against inflation amid the global monetary tightening vortex that is expected to remain very tense all through 2023. The stock market is worried about those medium-term difficulties and the large capital inflow from professional investors is almost lying dormant, causing a sharp drop in liquidity and a failure to increase stock prices as in the past.