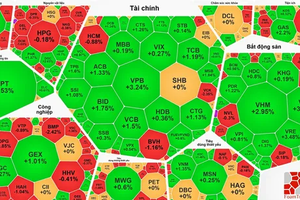

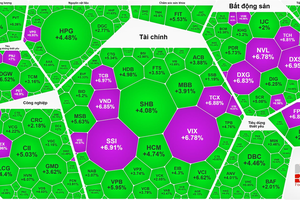

Room to increase

Many investors often evaluate the investment opportunities in the market by observing the VN Index. It is not really wrong to do so, but it does not always work. During the months of May and June, there was no clear bullish wave when the VN Index was still unable to break through the peak in January 2023.

|

In other words, if you look at the VN Index the stock market is still only accumulating by a wide margin after hitting a long-term bottom in mid-November last year. Also because of the market prediction based on the VN Index, it can be explained that the VN Index only increased to the threshold of about 1,200 points, equivalent to a 50 percent recovery rate compared to the decrease in 2022.

This year the stock market is not like many times in the past when the cash flow was withdrawn while the economic growth prospects slowed down, businesses faced difficulties, and there was the pressure of corporate bonds. When cash flow weakened and combined with a significant increase in outstanding shares through additional issuance then within the last two months, or rather the first six months of the year, the cash flow came from individual investments and speculative opportunities to create waves.

This has been proven by a series of extremely good stocks, even having doubled in value in just six months from the bottom. The two main reasons why many stocks recovered spectacularly were the expectation of improved business results, and also cash flow began to pour into the stock market after the interest rate dropped continuously. But it will be difficult to gauge whether such bullish expectations are justified, as this is a time for enthusiastic investors, especially those driven by the fundamentals of the business.

However, when the second quarter profit numbers appear, it will be confirmation of those expectations. Therefore, the closer to the time the financial statements are released, the more cautious and realistic investors become. It is not that investors are disappointed with the numbers, but simply that the price has risen before, and now it is time to revalue expectations.

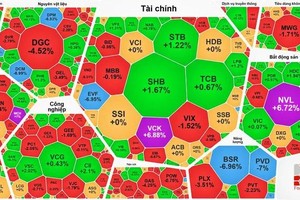

Risks decreasing

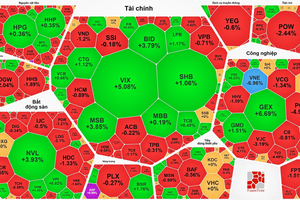

The newly released second quarter macro data confirms the expectation of economic recovery. The GDP in the second quarter of 2023 grew by 4.14 percent, higher than the increase in the first quarter of 2023 of 3.32 percent. This is a sign that there is a very high possibility that growth has bottomed out in the first quarter of 2023. In the last three quarters of 2022, the stock market plummeted due to the risk of a decline in growth in the next quarters, and the stock hit bottom in mid-November 2022, despite the growth figure for the whole year of 2022 being at 8.02 percent but actually decreasing quarterly. The situation can be repeated now but in the opposite direction, when the worst has appeared in the first quarter of 2023 and improvement has appeared in the second quarter of 2023, it is possible that the outlook continues to improve in the next quarter.

However, the stock market relies not only on expectations but also on the fact that this year the macro growth will be low. The target of 6.5 percent growth is difficult to achieve when the first half of 2023 growth is only 3.72 percent. This makes the stock market deduce in two directions. The conservative direction may be cautious with the market outlook because low economic growth inevitably causes the market to have a reasonable and commensurate valuation, which means it is difficult to grow strongly, especially when corporate profits will not be as good as last year. The optimistic direction can be that to promote growth many stimulus and support measures will have to be deployed. The clearest evidence is the fourth consecutive interest rate cut from mid-March until now and the stock market has always benefited from monetary easing trend.

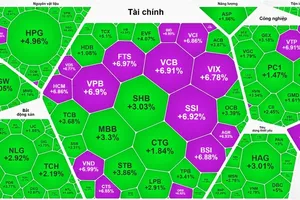

The stock market is showing a clear effect of low-interest cash flow. Statistics show that the level of transactions on the stock market has increased significantly after interest rates dropped. Specifically, the average total matched value in March 2023 of the two exchanges HoSE and HNX hit the bottom with about VND 8,786 bln per session. By April 2023 it increased to VND 11,057 bln per session, in May 2023 it reached VND 12,160 bln per session and last June it was VND 16,919 bln per session. The average liquidity threshold of June 2023 was equivalent to the period of March and April 2021, before the market entered the trading boom period.

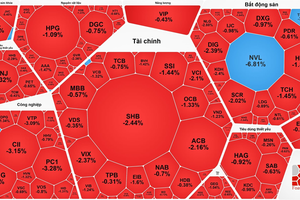

However, cash flow is not the only factor that pushes up the stock market. The volume of shares outstanding is now much larger than in 2021, which means that the weight is greater even at the same price. On the other hand, it is not just speculative individual cash flow that can make waves, but institutions are more concerned with fundamentals. The ability of enterprises to absorb capital is extremely weak when credit growth as of 4 July 2023 was only 4.2 percent. Most of the businesses have bad credit quality that is not enough to meet the loan conditions, and the other part has no need to expand production so there is no need to borrow. These are negative signs for corporate earnings prospects.