Illustrative photo

Illustrative photo

Slight increase in rate

Vietcombank recently increased deposit interest rate by 0.2% for term less than twelve months, after maintaining a lower level since the beginning of the year. Among group of joint stock commercial banks, VPBank also increased the deposit interest rate by 0.2%, for six-month term to 4.5% to 5% per year, and for twelve-month term to 6% to 6.5% per year. Earlier in the month of May, Sacombank, Techcombank, and TPBank also increased deposit interest rates, as did NCB and BacABank.

In the interbank market, interest rates also moved up. From 17 June to 24 June, interbank interest rates simultaneously increased in all three types overnight, namely, one-week term, two week term, and after three weeks, at previous downward adjustment. The increase is 0.26% on 1.21%, 0.24% on 1.41% and 0.29% on 1.74% per year. This interest rate move is attributed to the fact that commercial banks have limited the supply of the Vietnamese dong, as credit growth has recovered in the last six months, but capital mobilization was slower than in previous years.

Statistics from the State Bank of Vietnam show that in the first four months of the year, the amount of money deposited into credit institutions only increased by about VND 120,000 bn, an increase of 2.34% compared to the end of last year, the lowest increase in six years and only half that compared to pre-Covid pandemic period. As of 21 June, the General Statistics Office announced that the capital mobilization of credit institutions has increased by 3.13%. While in 2020, capital mobilization in credit institutions increased by 4.35%, in 2019 by 6.09%, and in 2018 by 7.76%.

Total means of payment as of 21 June increased by 3.48% compared to the end of 2020, along with the growth rate of deposits lower than the growth rate of credit balance and lower than the average deposit growth rate in the same period. In previous years, it was seen that the money flowing out of the credit institutions into circulation was higher than the money flowing into banks.

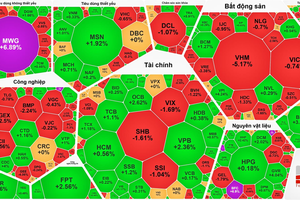

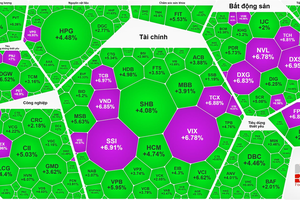

Stocks more lucrative

According to a report of the General Statistics Office, there is data that can trace this cash flow path. According to the report, by the end of May, the total capital mobilization for the economy in the stock market was estimated at VND 116.400 bn, up 68% over the same period last year. This total deposit doubled in just two months. By the end of March, the total capital mobilization in the stock market was only about VND 55,562 bn.

According to Dr. Nguyen Tri Hieu, a financial expert, with low-interest rates investors are pouring money into securities, instead of saving money in banks. This is seen in the fact that a majority of investors who recently joined the stock market are not professional or institutional investors. The number of new accounts opened in May increased sharply to 114,000 accounts, which is the highest ever. The number of new accounts opened in the first five months of 2021 exceeded the number of accounts opened in the whole of 2020. According to Rong Viet Securities, this is completely reasonable when deposit interest rates are still low while the lucrative profitability in the stock market cannot be denied or ignored in recent times.

Mr. Nguyen Son, Chairman of the Vietnam Securities Depository (VSD), said that in the context of stable interest rates at a relatively low rate, it is possible that the cash flow from individuals who previously invested in other fields is now temporarily in securities, creating a bullish effect in the market. Meanwhile, the Ministry of Construction pointed out that part of the cash flow is moving into the real estate sector because this is an investment channel that is considered safe and has many future development opportunities, in the event when stocks, gold, or foreign currency becomes unstable or trading at a high level, and low deposit interest rates are no longer enough to attract idle money.

Idle money flow

Low-interest rates have weakened savings deposits. Idle cash flows from places with low interest rates in banks to places with higher interest rates, such as the stock market. Hence, not only has idle money moved out of banks, but even credit lines of banks have gone into these areas. According to Mr. To Giang Nam, Investment Director at Vietinbank Capital, in addition to money sources from foreign investors, ETFs, and F0s, the main cash flow that promotes the growth of the stock market, in large part comes from borrowed money, especially margin activities.

At the end of the first quarter, the margin balance of securities companies granted to investors was about VND 101,000 bn, an increase of 53% compared to the same period last year and an increase of more than 25% compared to the previous quarter. Most of the cash flow of securities companies on margin loans comes from loans from banks. In addition, securities companies have the capital for margin lending from raised bond issuance.

According to the State Bank of Vietnam, it is estimated that by the end of June, agricultural and rural credit is estimated to increase by 4.8%, small and medium-sized enterprises by 3.9%, exports by 9%, support industries by 6.94%, and high-tech application enterprises by 14.5%. Meanwhile, outstanding credit flowing into securities is expected to increase by 3% by the end of June, but it accounts for a small portion of about 0.48% of total outstanding loans of the economy, estimated at VND 46,700 bn, an increase of about VND 400 bn to VND 500 bn compared to the end of 2020. At the same time, in the first six months, real estate credit growth has slowed mainly due to the impact of the current wave of the Covid-19 pandemic. This has led to a sharp drop in investment activities. Real estate credit growth has been lower, averaging around 5.1%.

According to Dr. Nguyen Tri Hieu, many people borrow money for consumption purposes but then they use this money to invest in securities. Therefore, the reported data is not actually very reliable. Credit capital currently accounts for at least 60% of capital sources in the stock market and real estate, which is part of the reason why these markets have grown so strongly in recent years. According to economic law, the movement of idle cash flow into the economy when interest rates are low is a very normal occurrence. However, if the heat of markets, such as on stocks, is fueled by the influx of credit, then extreme caution should be exercised.