Simultaneously, investors were urged to refrain from engaging in this form of trading on the stock market without the requisite permissions from regulatory authorities. But is it justified to restrict the use of digital technology platforms that have been on the rise?

"Old for him but new for me"

|

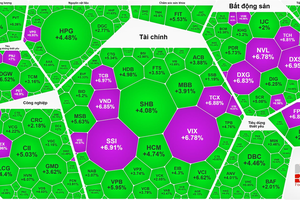

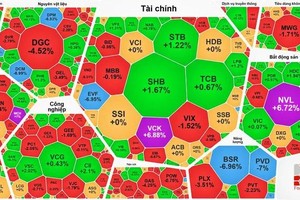

Robot trading, or high-frequency trading (HFT), has gained increasing popularity in international stock markets. In the US stock market, HFT accounts for approximately 50 percent of all trading, while in European markets, it constitutes roughly 20-30 percent of daily liquidity volume. This phenomenon extends beyond stock markets, as HFT transactions have become prevalent in commodity, foreign exchange, and cryptocurrency markets.

Although there are no official statistics available for robot trading in Vietnam's stock market, it is estimated to account for a relatively small portion of overall trading activities.

However, numerous organizations have been exploring ways to develop this technology. Common use cases for automated orders include creating financial products like warrants, derivatives, and ETFs, arbitrage trading, splitting orders, receiving orders from third-party collaborators with securities firms, copy trading, and risk management activities such as cutting losses and taking profits.

According to the State Securities Commission's official dispatch, if all these activities are classified as robot trading, the ban would encompass all transactions within the stock market.

Nevertheless, there exist diverse opinions both in favor of and against robot trading. Supporters argue that it is an inevitable trend, leveraging technology to advance finance. They believe that HFT's arbitrage trading enhances liquidity in the market. Conversely, opponents contend that HFT exacerbates market volatility, leading to extreme fluctuations due to trading algorithms.

Increased Convenience with Robot Trading

If robot trading is prohibited, the process of creating and executing orders would become more cumbersome compared to the efficiency of automated systems. Human intervention would be required for constant monitoring, rendering it nearly impossible to match the speed and accuracy of machines. However, not all trading activities on the floor necessarily rely on robotic execution, especially in futures contracts within the derivatives market.

One prominent form of robot trading is arbitrage, involving simultaneous buying and selling in both the underlying and derivative markets.

Given that there is typically a difference between the Vietnamese market's derivative and underlying assets, numerous arbitrage opportunities arise. Securities companies that embraced robot trading early on have reaped initial benefits and continue to do so. Banning robot trading could potentially hinder arbitrage trading, as opportunities can materialize rapidly, often outpacing human capabilities.

This could partially impact the liquidity of the underlying market (such as stocks in the VN30) and the derivatives market.

Order splitting, another common practice among some entities, occurs when a certain stock is artificially created to obscure real orders. Such activities have occasionally overwhelmed trading systems, necessitating solutions like increasing lot sizes from 10 to 100 to mitigate the issue. Banning robot trading may help limit system overload but is unlikely to significantly affect market liquidity. While there may be fewer orders, they could be more substantial.

Another form of trading involves receiving orders from third parties who collaborate with securities firms. In both the derivatives and underlying markets, securities firms not registered as underlying or derivative securities brokerage businesses may aggregate orders from their clients and execute them through collaborating securities firms, commonly referred to as receiving orders from a third party. If this type of trading isn't conducted using robots, it may need to be discontinued because large-scale operations would require real-time, machine-driven execution.

Copy trading and entrusted transactions on multiple accounts, recently introduced by some securities firms through robots, could become more challenging without automated trading. This shift may inconvenience securities firms, as manual execution may not meet the necessary speed and accuracy, potentially affecting liquidity.

With risk management trading, involving actions like cutting losses and taking profits, using robots allows investors to be more proactive, as these features are incorporated into certain modern trading software. This not only aids investors in managing risk but also contributes to market stability by preventing mass sell-offs, thereby reducing market volatility.

The decision to ban robot trading will undoubtedly impact market liquidity in the short term, although it may not be immediately apparent due to the relatively small proportion of robot trading on the stock market. Some machine-driven trading activities can still be executed manually. However, this move is expected to reduce market volatility in the near future. Certain operations will become more challenging without automated assistance, potentially affecting securities companies and financial industry stakeholders.

It is undeniable that the State Securities Commission's decision can mitigate overall market risks and volatility. Nevertheless, HFT remains a global trend. Hopefully, as Vietnam's stock market implements the KRX trading system and finalizes its management plan to stabilize the system and the market, regulatory agencies will gradually ease these restrictions. In doing so, the Vietnamese stock market can strike a balance between operational stability and the technological advancement of market transactions.