Chart: P/E ratio dropped sharply but Q2-2021 business results are good, while market forecasts a decline in P/E Q3 business results due to prolonged Covid.

Chart: P/E ratio dropped sharply but Q2-2021 business results are good, while market forecasts a decline in P/E Q3 business results due to prolonged Covid.

Investors eye Q3

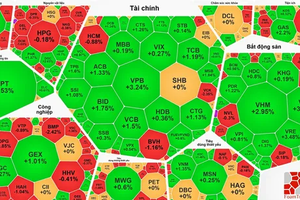

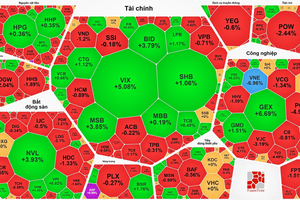

The second quarter business results of 2021 also saw some surprising figures as well. According to a total of about 700 enterprises of VNDirect Securities Company (SSC) that announced the second quarter profits, the net profit of these enterprises on all the three exchanges, namely, HoSE, HNX, and UpCOM, have increased by 66% over the same period last year. In the first six months of 2021, the net profit of enterprises on all three exchanges increased by 75.3%, over the same period last year.

When updated with new business results, the stock market's P/E ratio immediately decreased significantly. Specifically, at the historical peak on 2 July, the VN-Index reached 1420.27 points, and P/E ratio was about 19.3 times, according to Bloomberg data. At the bottom of the correction on 19 July, the P/E ratio was about 17.1 times. On 4 August, when VN-Index recovered to about 7.3% from the bottom, the P/E ratio continued to drop by 16.8 times. The fact that the VN-Index recovered but P/E ratio continued to decline was due to the business results of listed companies on the index. The entire business results are not yet available, so it is likely that the P/E ratio of the Vietnamese stock market will continue to decrease in coming time.

In reports analyzing the prospects of Vietnam stock market for securities companies, the valuation through this P/E index is being considered much more attractive than other markets in the region. This is a long-term advantage, but does not always signal a price growth opportunity. It is a fact that the P/E of the Vietnamese stock market is always lower than that of the region, but these are still normal ups and downs. On the other hand, P/E ratio has also shown a significant deviation in correlation with Foreign Indirect Investment inflow during the last twelve months, when Vietnam's stock market was considered attractive with low P/E, but foreigners have still been net withdrawing.

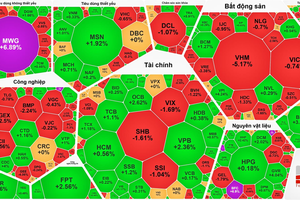

The Vietnamese stock market peaked in early July before the second quarter earnings reports appeared with a much higher P/E ratio than at the end of July and early August. Many stocks also peaked at the beginning of July, some even peaked from June and then corrected down. The analysis is that investors do not attach importance to published profit numbers because the present quickly becomes the past. Fundamentals are always reflected first due to expectations, so even P/E ratios can predictably drop to attractive levels.

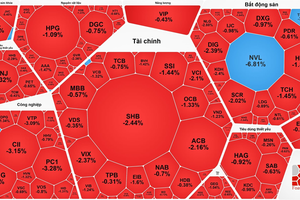

When looking at fundamentals at the moment, the market is very attractive. However, the market situation shows another aspect, which is that the market is not looking at the present. Although VN-Index is on the way to recovery after reaching a historic peak in early July, the cash flow is clearly exiting the market. Specifically, during the recovery period from 19 July to now, the matched order volume on HoSE has only averaged VND 16,748 bn per session, while the average level in June reached VND 22,224 bn per session, and even in the first half of July it reached VND 21,182 bn per session.

What has kept the fundamentals underwhelming for investors, despite the market's recovery, is evidenced by a steep drop in daily trading volume, which is worrisome for a tough future. The third quarter of 2021 is the phase that investors care about much more now.

Difficult third quarter

Impressive Q2-2021 business results are in the context that the economy in general and production and business activities have not yet been affected by the fourth wave of the Covid-19 pandemic. In all macro growth and valuation scenarios of the stock market, the forecast for the third quarter business results of listed companies and organizations must all revolve around the possibility and ability to control and contain the fourth wave of the Covid-19 pandemic.

After optimistic comments were made at the beginning of the year and even in the second quarter of 2021, many international and domestic organizations are adjusting their plans to reflect the risks of a new wave of Covid pandemic occurrences. The growth scenarios are uncertain, by assuming when exactly the pandemic will be under control.

For example, the Institute for Economic and Policy Research (VEPR) proposes a scenario where the pandemic can be controlled by August, and the growth for the whole year in 2021 will also be in the range of 5% to 6.1%. The bad scenario reflects that the pandemic will only be controlled by the fourth quarter, and the growth rate is being seen at 3.5% to 4%. ADB has revised down its 2021 growth forecast from 6.7% to 5.8%, when there is a variable about the fourth wave of Covid-19. Several securities companies have also revised down their growth forecast in their recent August report.

Investors all understand that forecasts will have errors in the stock market, and there will be adjustments when new variables appear. The problem is that the Covid-19 pandemic containment variable is too difficult to predict, due to its complicated nature. If based on the past, as during the first quarter and the second quarter of 2021, the profits of enterprises have decreased significantly. So the current low P/E ratio on a profit basis of the first two quarters of the year won't be really cheap anymore. According to the law of expectations, cash flow declines because investors are not looking at the good picture of the second quarter but are waiting for the dark areas of the third quarter to show up, or at least until the basis for more sure and certain expectations appear.