|

Although there are now many positive signs in the global market, it will take more time to verify the situation and effort must be maintained to avoid the situation from worsening.

Protecting domestic currency

The market received the first interest rate hike in 2023 by the FED quite objectively. The expected increase of 0.25 percentage points helped the global stock markets to stabilize and even increase in February 2023. Domestically, the interest rate level did not see noticeable developments, with the exchange rate even cooling down.

By mid-February, there started to appear a reduction in deposit interest rates initiated by large commercial banks, namely, Agribank, Vietcombank, BIDV, and Vietinbank. The 12-month term deposit interest rate was adjusted down to about 7.4 percent per year. Although for smaller joint-stock commercial banks, the equivalent term deposit interest rate is still in the range of 9 percent to 9.3 percent. The big four banking group of Agribank, Vietcombank, BIDV, and Vietinbank with a credit market share of 45 percent are leading the trend, and the interest rate race is very unlikely to occur.

It is certain that the FED will have more rate hikes, even if only in small amounts, but it will still create some pressure. The important thing is that if the pressure on the domestic exchange rate is not great, the pressure on interest rates will also cool down. The recent increase in monetary interest rates has been more protective of the domestic currency than in an effort to curb inflation.

Another measure also taken by the State Bank of Vietnam is to sell US dollars to recover the Vietnam dong. Therefore, when the US dollar cools down, the State Bank of Vietnam will have conditions to buy back the US dollar, to offset foreign exchange reserves and to contribute to more cash flow to increase liquidity and reduce interest rate pressure. An estimate by VNDS Securities Company said that the State Bank of Vietnam has bought about US$3.6 bln since the beginning of 2023. Interbank interest rates have dropped from more than 6 percent per year at the end of January 2023 to below 5 percent per year by February 2023. The interbank overnight interest rate in the normal period of 2019 was around 4 percent per year.

Inflationary variables remain and the FED may continue to pressure interest rates globally. However, if the situation is not unusual, the FED is expected to have two more rate hikes in March and May and each time of 0.25 percentage points. In the second half of 2023, progress on rate hikes will come to a halt. In other words, the market is seeing a clear path and a visible target, which is to expect the biggest pressures to disappear. According to VNDS, the domestic deposit interest rates may peak in the first quarter of 2023 and cool down from the second quarter of 2023. It is forecast that the average deposit interest rate for the 12-month term will be only 7.5 percent per year by the end of 2023. This level is also equivalent to the period held in 2019.

Corporate profits

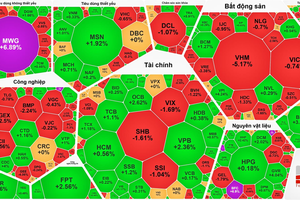

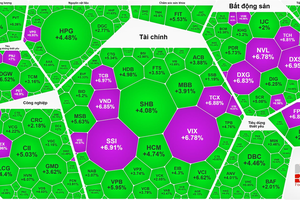

Business results of the fourth quarter of 2022 ended with a downward growth trend as expected. According to statistics of VNDS, the total net profit in the fourth quarter of 2022 of companies listed on three exchanges, namely, HOSE, HNX, and UPCOM decreased by 30.4 percent over the same period, the biggest drop since the outbreak of the Covid-19 pandemic.

In terms of structure, enterprises in the VN30 blue-chips group had the lowest decline in net profit growth in the fourth quarter of 2022, at negative 11.5 percent, while the mid-cap fell to minus 64.8 percent, and the small-cap was negative at 83.3 percent. The factors affecting the profit in the fourth quarter of 2022 are forecast to continue to persist at least in the first quarter of 2023, but with better performance in the group of large enterprises the opportunity for this group will remain. Profit is also the highest. This was also reflected in the stock price when most of the VN30 stocks had a slight correction than the rest, which was the reason for the slow decline of the VN Index.

This is also the basis of the expectation that the Vietnam stock market had really bottomed in November 2022, and the current short-term correction has little risk of pushing the VN Index to penetrate bottom. Of course, each stock will have different correction levels, but as long as the blue chips can stabilize the Index, the main trend of the market is still accumulation for a new cycle. How long the accumulation will last needs to look at the signs of the fundamental factor. For the macro, it is the interest rate that peaked and turned down positive credit growth, or business dynamics that are clearly reflected on indicators such as PMI or import-export turnover.

From a micro perspective, enterprises may announce a less satisfactory profit figure in the first quarter of 2023, but if the decline in revenue and profit slow down, the chances of recovery in the remaining quarters of 2023 are clear. The stock market can wait for an official number, even a bad one, to project a better expectation in the future. The reality is that the stock market always bottoms out when the expected risk is highest, not when the economic data is at its worst.